A sluggish quarter for Klang Valley’s residential property market

The residential property market in the Klang Valley is still very soft due to the prolonged impact of the pandemic, economic slowdown and negative sentiment in general, which have led to fewer transactions, says Savills Malaysia director of research and consultancy Amy Wong.

“Some new launches, however, were selling well during the quarter, such as Edelweiss at Tropicana Gardens. The sales rate has increased from the previous quarter,” she says in presenting The Edge | Savills Klang Valley High-Rise Residential Property Monitor for 1Q2021.

Meanwhile, some property developers have reported improved sales, especially for residential projects in the affordable price range in prominent areas of Kuala Lumpur as well as well-located townships in Selangor, such as Bruce On 9 and Audrey On 9 at Emerald 9 Cheras, You City 3, Emerald Hills Lakefront Condo (South Tower) and Majestic Maxim in Cheras.

To help stimulate the property market, the government has introduced several initiatives, including low interest rates, says Wong. “The government has extended the Home Ownership Campaign (HOC), which was set to expire in May, to the end of 2021. This is good news. Exemptions for stamp duty on instruments of sale as well as loan funding caps of more than 70% will primarily favour first-time homebuyers.

“First-time buyers, those looking for larger spaces and investors who took a wait-and-see stance in 2020 due to the uncertainties will be able to take advantage of the HOC rewards until the economy shows signs of recovery.

“The full stamp duty exemption on the memorandum of transfer and loan agreements is applicable to first homes priced below RM500,000 for agreements signed between January 2021 and December 2025, as part of Budget 2021’s extension of incentives for the property industry,” Wong notes.

In addition, the allocation of RM15 billion under Budget 2021 to revive and ensure the continuity of mega projects, such as the Mass Rapid Transit Line 3 (MRT3) in the Klang Valley and the Klang Valley Double Tracking Project Phase 1, is expected to improve the real estate industry, she says.

“Collaterally, these mega projects would supplement nearby residential and commercial developments and stimulate more rural growth, resulting in a significant economic boost.

“To that end, the government’s steps in Budget 2021 to expand employment opportunities, concentrate on training and upskilling employees, provide wage subsidies to keep jobs and incentivise businesses to recruit local labour will help boost consumer trust in the coming year.”

Wong notes that according to Bank Negara Malaysia’s Financial Stability Review 2020, released in October last year, banks’ credit costs could grow to RM29 billion (which is equivalent to 1.4% of total loans) over 2020 and 2021.

“These figures were calculated using a conservative estimate of the percentage of loans eligible for targeted repayment assistance. Given that the pandemic has already had a major impact on corporate profits and national GDP growth, consumer trust and purchasing behaviour will be shaped by job and financial security in the future,” she says, adding that the country’s GDP contracted by 4.5% last year. “Furthermore, Bank Negara reduced the overnight policy rate four times last year to a new low of 1.75% since September 2020.”

Meanwhile, the ongoing rollout of vaccination programmes in many countries, combined with policy support, will help boost private demand and strengthen labour market conditions, says Wong.

“Although financial markets have been volatile, economic growth has been supported by financial conditions. The risks to the growth outlook have decreased significantly, but remain on the downside, owing to uncertainties about the course of the Covid-19 pandemic and the efficacy and timely rollout of vaccination programmes.”

In the KLCC, Bangsar and Mont’Kiara segments of the Kuala Lumpur property market, activities were still very sluggish in 1Q2021, she says. “However, there was no significant drop in prices reported and no new launches were seen during the quarter in review,” she notes, adding that the price movements of the sampled properties remained minimal.

Compared with 4Q2020, capital values of the selected samples in the KLCC area increased by 1% on average, whereas those in Bangsar decreased by 0.4%. Meanwhile, the capital values of the samples in Mont’Kiara remained unchanged.

In the Selangor property market, Subang Jaya, Bandar Sunway and Petaling Jaya experienced a quiet secondary market, similar to Kuala Lumpur, says Wong. “Although competition from the primary sector had triggered this effect by offering buyers more options and a lower entry cost to property ownership, the Covid-19 outbreak and movement restrictions negatively impacted these plus points.”

The capital values of sampled properties in Subang Jaya remained relatively stable during the quarter, she notes. “Petaling Jaya showed a slight increase while Bandar Sunway showed a decrease in capital values.”

The asking prices of the sampled properties had begun to show a downward trend compared with the previous quarter, she adds.

Meanwhile, Wong has observed developers advertising their sales turnaround to reassure potential customers during this uncertain period and that most of the construction activities had resumed during that round of Movement Control Order (MCO). “However, due to last year’s MCO, all planned vacant possession and project completion will be delayed,” she says.

Stagnant activity across Kuala Lumpur

In the KLCC area, both the primary and secondary markets remained slow in 1Q2021. The sampled 2-bedroom units in the area saw a few transactions on the secondary market last year, which was published in this quarter’s Valuation and Property Services Department’s (JPPH) sales data, says Wong.

Both the capital values and average asking prices of the sampled properties in the KLCC area were 1% higher in 1Q2021 compared with the previous quarter. However, year on year (y-o-y), the average capital value had fallen 4% to RM1,117 psf in 1Q2021 from RM1,161 psf in 1Q2020. The average asking price in the KLCC area, based on the sampled properties, dropped 1% y-o-y to RM1,247 psf in 1Q2021 from RM1,260 psf in 1Q2020.

There were no property launches in the KLCC area during the quarter in review, she observes.

In Bangsar, the high-rise residential property sector was also slower, says Wong. “Compared with 2019, the number of secondary market transactions for the sampled 2-bedroom properties fell by half last year.”

Only one transaction each was reported in Sri Penaga, Cascadium and Suasana Bangsar in 4Q2020. The transactions were published by JPPH in this quarter’s report, Wong notes.

According to her, property prices in Bangsar remained unchanged during the quarter in review, but the average asking price was lower than in the previous quarter. The average asking price of the sampled 2-bedroom units in Bangsar fell 0.4% quarter on quarter (q-o-q) to RM984 psf in 1Q2021 from RM988 psf in 4Q2020.

In Mont’Kiara, the average capital value of the sampled 2-bedroom properties remained stagnant during the quarter, falling by less than 1% to RM591 psf from RM596 psf in 4Q2020. A y-o-y comparison shows that the average capital value had decreased a significant 4.3% from RM618 psf in 1Q2020. The average asking price in Mont’Kiara had stayed consistent on a q-o-q basis at RM683 psf.

According to Wong, the availability of high-rise residential properties in Mont’Kiara had increased as several projects were recently launched. Examples include Allevia Mont’Kiara and The Fiddlewoodz at KL Metropolis, which will add 294 and 679 units respectively to the market.

Lower asking prices in Selangor

According to JPPH data, there were very few transactions of 2- and 3-bedroom properties in Subang Jaya, notes Wong. “As a result, the average capital value of the sampled properties remained unchanged during the quarter in review at RM539 psf.”

Meanwhile, the average asking price in Subang Jaya decreased by 2.4% y-o-y to RM577 psf in 1Q2021 from RM591 psf in 1Q2020.

Alira Metropark Subang is a new freehold development that is expected to add 836 units of serviced apartments and low-rise villas to the Subang Jaya property market in two years, she says.

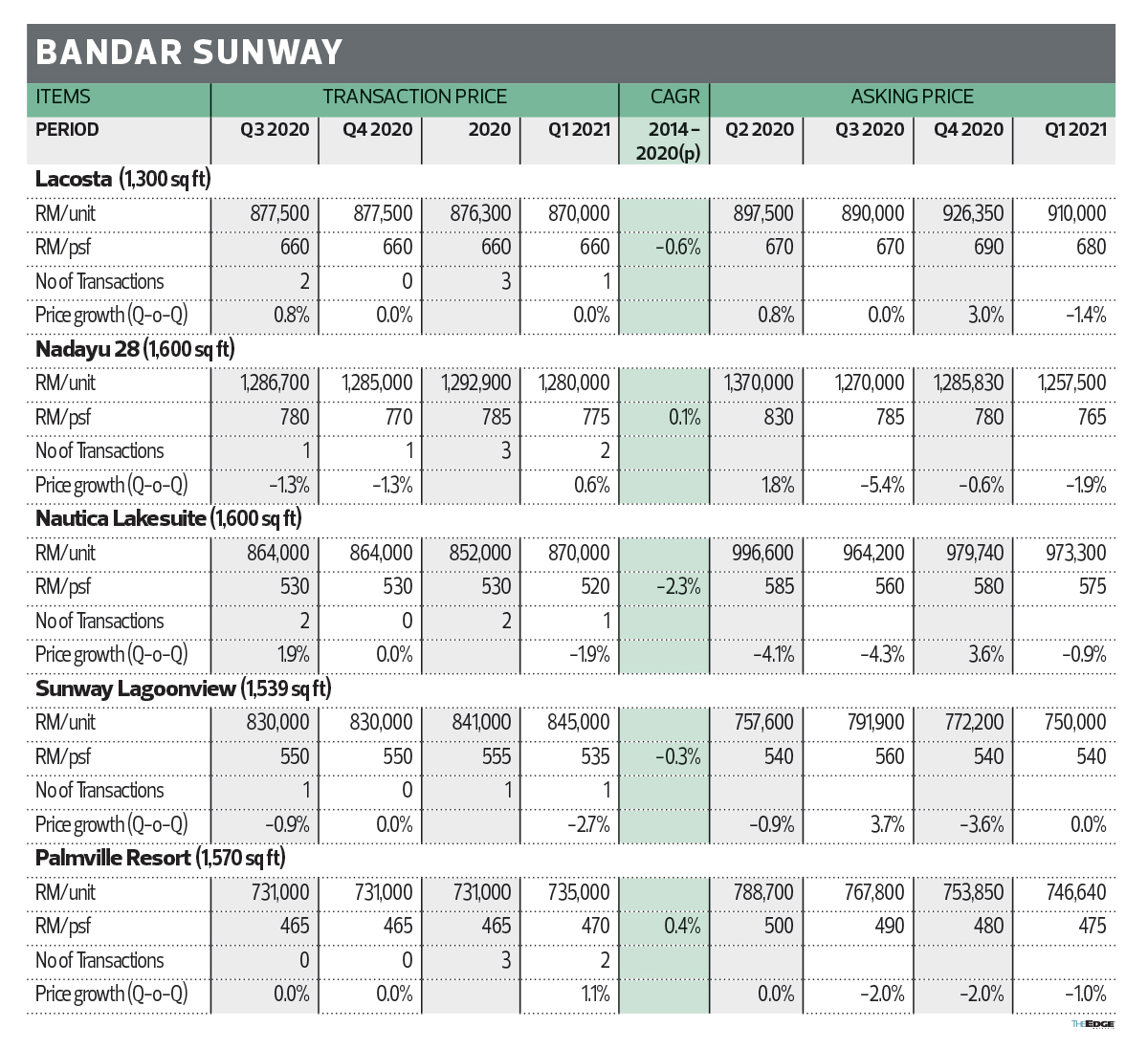

In Bandar Sunway, the average capital value of the sampled properties decreased marginally q-o-q due to a decrease in transaction price per sq ft in 4Q2020, which was reported during the quarter in review, says Wong.

Three-bedroom units in Bandar Sunway, ranging from 1,300 to 1,600 sq ft, recorded an average capital value of RM592 psf during the quarter — a 0.5% decrease from the RM595 psf in 4Q2020.

According to Wong, the average property price per sq ft in Bandar Sunway had decreased y-o-y. In contrast, the average capital value of LaCosta and Palmville

Resort Condominium increased by 0.8% and 1.1% respectively. Meanwhile, the average asking price in Bandar Sunway fell by 1.1% q-o-q to RM607 psf.

In Petaling Jaya, several secondary market transactions were registered in 3Q and 4Q last year, which were published by JPPH this quarter, she says. Meanwhile, the average capital value had risen to RM634 psf.

“With about nine developments expected to be completed soon, Petaling Jaya is more competitive than Subang Jaya and Bandar Sunway. Due to the extension of the HOC until end-2021, this region will continue to see steady growth in terms of new unit take-ups,” says Wong.

Edelweiss at Tropicana Gardens stood out from the crowd, she says. “Its take-up rate increased to 33% during the quarter in review from 17% in 4Q2020. One of its unique selling points is its connectivity to Tropicana Gardens Mall and the Surian MRT Station.”

As for the average asking price in Petaling Jaya, that of the sampled 2- and 3-bedroom properties with built-ups of 1,100 to 2,000 sq ft fell 0.3% to RM641 psf from RM643 psf in 4Q2020.